When looking to start a business or protect investments you have several options in the type of entity you can form. As with anything, there are advantages and disadvantages to limited liability companies.

Advantages

- It limits liability for managers and members.

- Superior protection via the charging order.

- Flexible management.

- Flow-through taxation: profits are distributed to the members, who are taxed on profits at their personal tax level. This avoids double taxation.

- Good privacy protection, especially in Wyoming.

- This is a premier vehicle for holding appreciating assets, such as real estate, stock portfolios, and intellectual property.

- Extraordinary flexibility in the ability to allocate profits and losses to members in varying amounts.

Disadvantages

- Some states, including California, charge extra fees for operating an LLC.

- Income splitting is available, but unlike an S Corp, in a business operating as an LLC all income may be subject to payroll or self-employment taxes.

- Some states do not allow professional groups (i.e., doctors or dentists) to operate through an LLC.

- Transferability restrictions – consent of membership is required for each and every transfer of membership interests. (This can also be a plus.)

- Single Member LLCs face reduced asset protection. Many states do not honor asset protection for LLCs with a single owner.

LLCs and the Charging Order

One of the great asset protection advantages of the LLC is the charging order.

Charging order protection arises from each state’s law and is a key strategy for shielding your assets from attack. As with anything in the law, the charging order is subject to change and interpretation by the courts. Some states view the statute differently than others, which is why it is important to choose the right state when forming a limited partnership (LP) or limited liability company (LLC). It is also important to keep up on the new court cases and trends in this area to keep yourself better protected. Remember, the LLC has only been widely used in the USA in the last 25 years or so. We are just now starting to see court cases defining their scope and use.

Going back to the original statute (the rule passed by each state’s legislature) we consider section 703 of the Uniform Limited Partnership Act. It states that if a partner of an LP owes money to a judgement creditor (one who has gone to court and prevailed) the court may order a ‘charge’ against the partner’s interest to pay the judgement creditor. Thus the term ‘charging order’. This rule also applies to LLCs.

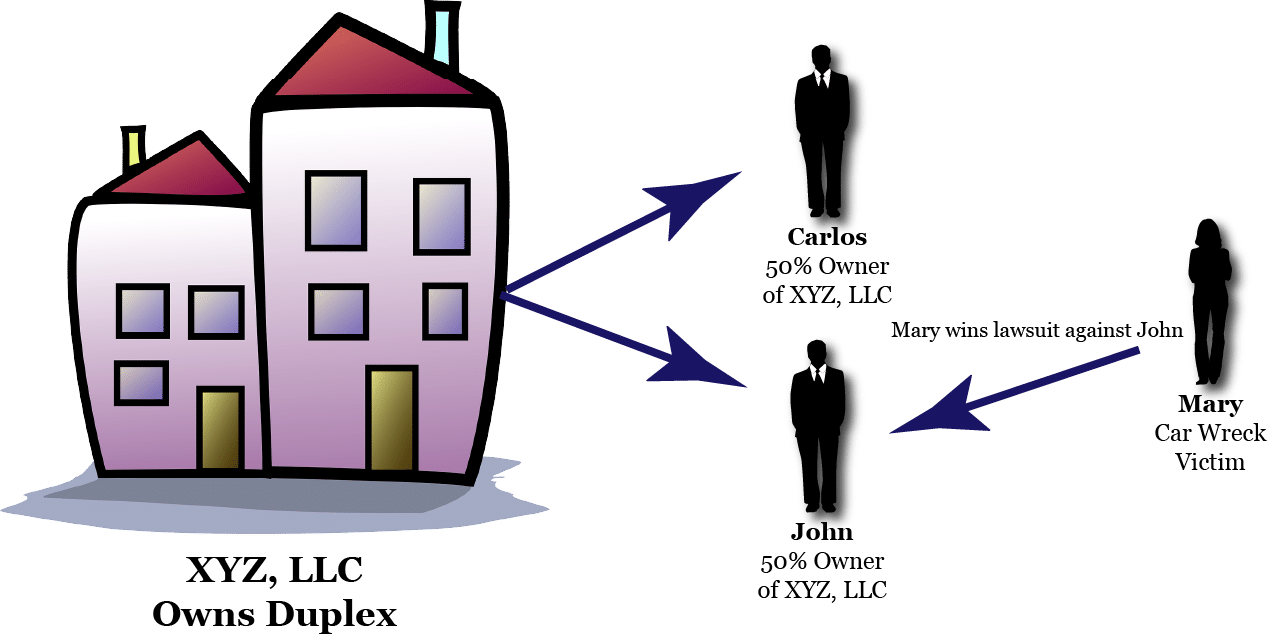

For example, if John owns a 50% membership interest in XYZ, LLC and John owes money to Mary after losing to her in court, Mary can seek a charging order to receive John’s 50% share in the distributions from XYZ, LLC. Of course, John’s other partner Carlos is not as keen to this, but any disruption is minimized with the charging order. Mary does not step into John’s shoes as a substituted partner. She can’t vote and tell Carlos how to run the business. Instead, she is only assigned the distributions that would have been made to John.

Again, the charging order is a court order providing a judgement creditor (someone who has already won in court and is now trying to collect) a lien on distributions. A chart helps to illustrate our example:

In our example, John was in a car wreck which injured Mary, the other driver. Mary does not have a claim against XYZ, LLC itself. The wreck had nothing to do with the duplex. Instead, Mary wants to collect against John’s main asset, which is a 50% interest in XYZ, LLC. Courts have said it is not fair to Carlos, the other 50% owner of XYZ, to let Mary come crashing into the LLC as a new partner. Instead, the courts give Mary a charging order, meaning if any distributions (think profits) flow from XYZ, LLC to John then Mary is charged with receiving them.

Mary is not a partner, can’t make decisions or demands and has to wait until John gets paid. If John never gets paid, neither does Mary. The charging order not only protects Mary, but it is a useful deterrent to frivolous litigation brought against John. Attorneys don’t like to wait around to get paid.

This short video also explains the charging order:

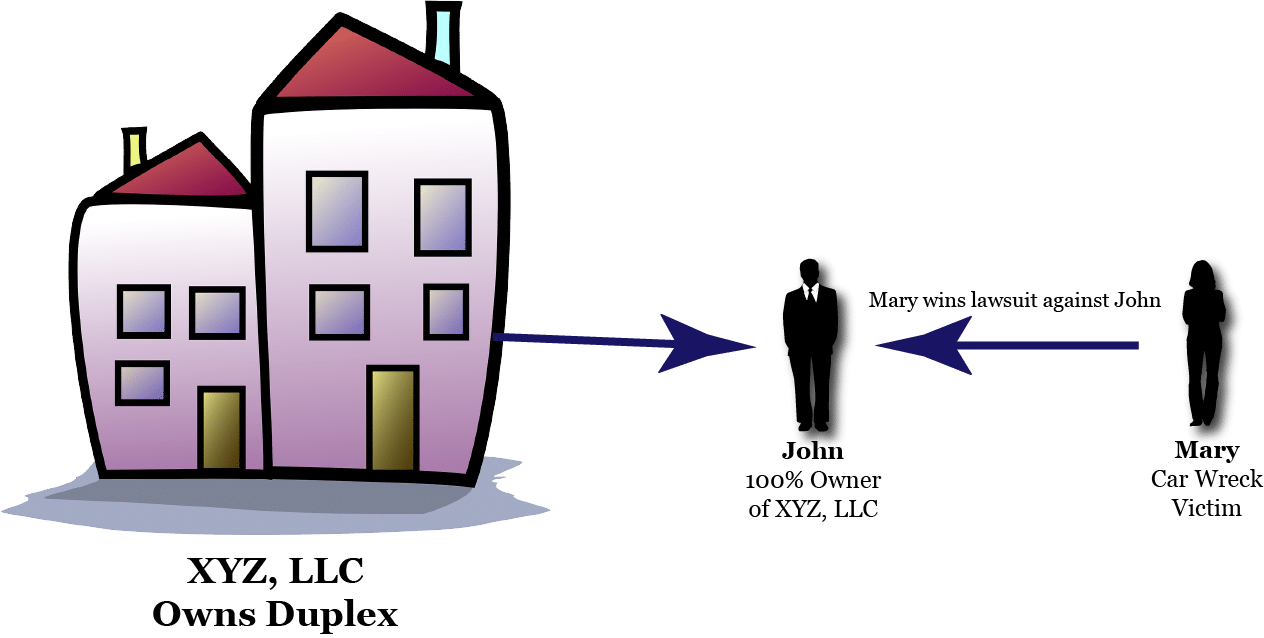

But what if there is only a single owner?

The Difficulties of Single Member LLCs

In a Single Member LLC, there is no Carlos to protect. It’s just John. Is it fair to Mary to only offer the charging order remedy? Or should other remedies be allowed?

A key issue is whether the charging order applies to a single member (one owner) LLCs. There is a nationwide trend against protecting single member LLCs with the charging order. Courts are starting to deny single owner LLCs the same protection as multiple member LLCs. The reason has to do with the unique nature of the charging order.

In June of 2010, the Florida Supreme Court decided the Olmstead vs. FTC on these grounds. In a single owner LLC there are no other members to protect. The court allowed the FTC to seize Mr. Olmstead’s membership interests in order to collect. Other states have followed the trend.

How Corporate Structure Can Increase Protection

Say you have a property in Oregon. That property is entitled to an Oregon LLC, which is owned by a Wyoming LLC. You then invest in a property in North Carolina, so you set up a North Carolina LLC owned by the Wyoming LLC.

If a tenant of your Oregon property sues over something that happened on the property, they have a claim against the Oregon LLC, not against you personally. They can’t get at your North Carolina LLC, and they can’t get at equity held on your personal property.

As you can see it’s beneficial to spread your properties across multiple LLCs. If you have 10 properties all in one LLC, it becomes a target-rich LLC. Often, we recommend only having one property per LLC. You may wish to have two or three properties in an LLC, but it really depends on how much equity you have in each property. The structure of your business really comes in to play during an inside attack, which is where the lawsuit is against an LLC, not the owner.

In the case of an outside attack, where the owner of the LLC is the target of a lawsuit, the charging order comes into play. In our example above where Mary is trying to get at John’s property, let’s assume John is the owner of a Wyoming LLC, and he has LLCs in North Carolina and Oregon. The car wreck has nothing to do with John’s Wyoming LLC, the holding in Oregon or the holding in North Carolina, so Mary can only go after John. And since John has a Wyoming LLC, even if he is the sole owner of the Wyoming LLC, Mary’s only option is the charging order. If the Wyoming LLC makes no distributions, Mary gets nothing. If the Oregon LLC and the North Carolina LLC make no distributions to Wyoming, Mary gets nothing.

This is not a great situation for attorneys who are on a contingency fee. They get a percentage of what is collected and it’s not a really good way to operate if they have to sit around get a charging order against the Wyoming LLC and then sit around and wait to get paid. Attorneys, being rational, economic animals are going to take the next case that has insurance instead of waiting for John to pay Mary.

You want to use the strategic positioning of the Wyoming LLC, which will own all your other out-of-state LLCs. States like Oregon and North Carolina may not protect the single member LLC, so you really need a Wyoming entity for protection in a case like the car wreck example. The Wyoming LLC creates a firewall against attorneys and frivolous lawsuits.

Entity Structuring is Our Specialty!