You design a lot of things in your life. The layout of your house, the flow of your business, the requirements on your children, and many more scenarios are all elements of conscious design.

Asset protection is no different. There is an architecture, a cohesive structure, to your properly planned legal safeguards. Sometimes you try and do it yourself, which could be fine. Many people are into DIY. And yet, with all the asset protection misinformation on the internet, you’ve got to be careful. Does that overpriced ‘guru’ really know what they’re doing? You won’t know until the plan they’ve designed holds. Or fails.

Designing your asset protection plan does not improve with setting up more entities than you need. When your plan is solid with three LLCs, who benefits by adding 5 more LLCs to the mix? I know you will answer that question correctly.

Your effective design should never be a matter of confusion to you. If you don’t understand what your asset protection planner is suggesting, demand a clear explanation. If they respond that most attorneys and no clients will ever understand their ‘brilliant’ structure, get up and walk out. That’s not how it works. As well, if you ask to get a second opinion from another lawyer about the plan and they claim that no lawyer will even begin to comprehend what they’ve put together for you, as a special client and part of the elite inner circle, it is also time to leave. You need to clearly understand the plan. And so does your spouse.

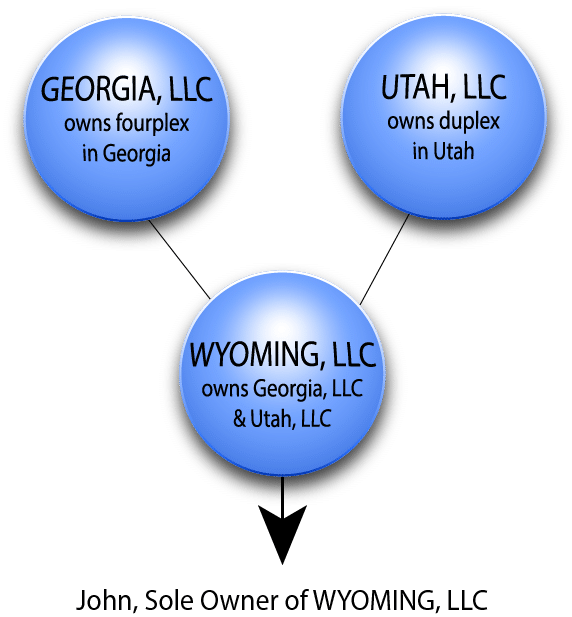

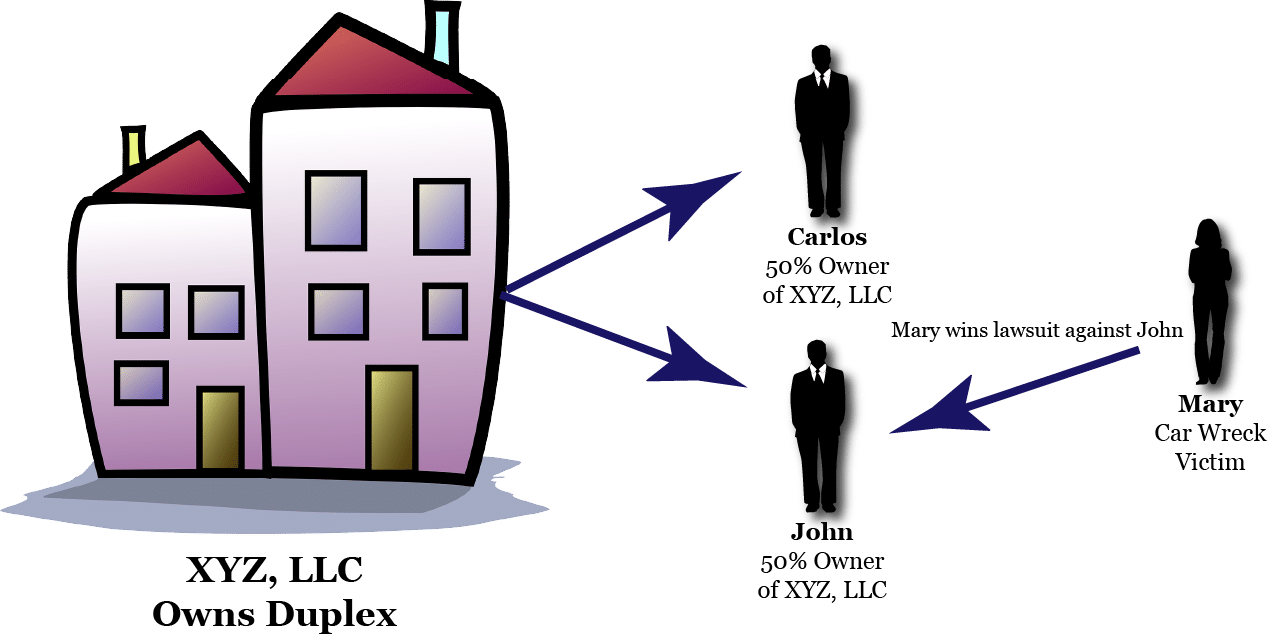

Sometimes, like an old bridge, a plan design has fault lines. The structure appears fine, until it collapses under pressure. This can be the case with land trusts. Promoters tout them for their asset protection benefits while they offer no such feature. To cover this inconvenient issue, they suggest that one or more land trusts be beneficially owned by one LLC. The structure appears as follows:

How will this structure hold up?

When a tenant in the duplex is injured on the property, they have the ability to sue the land trust for their damages. Some promoters claim that the tenant will never know the owner of the land trust because such information is confidential. Without exaggeration, this is one of the greatest legal fallacies in history. If the tenant’s attorney can’t locate the land trust owner all they have to do is publish notice of the lawsuit in the paper. It is very easy to do. And if the owner doesn’t respond to the lawsuit the tenant can win by default. You’ve lost the case and they are foreclosing on the property. “Well,” says the land trust promoter as they close shop and move 1,000 miles away, “I guess that didn’t work.”

Contrary to what these promoters may suggest, you don’t want to hide. You actually want to be found if needed, so that you can receive the notice of a lawsuit. You want to promptly turn the claim over to your insurance company so they can defend you and hopefully settle the case. If you hand them the claim after a default is entered in virtually all cases they don’t have to cover you. You didn’t give them proper notice of the lawsuit. Your design flaw is not their problem.

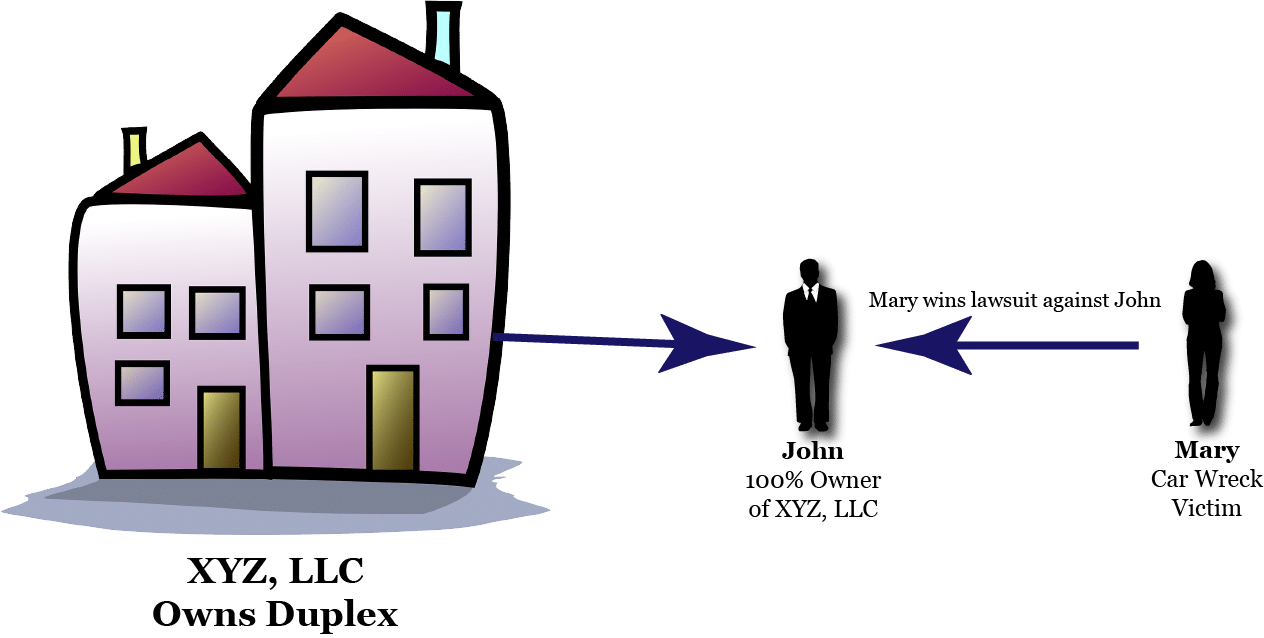

There is another design flaw in the structure above. Let’s say the promoter acknowledges that an LLC needs to be in the mix for its benefits of limiting liability. So, the beneficial owner (a required feature of land trusts and akin to a shareholder in a corporation or a member in an LLC) is listed as XYZ, LLC. When Land Trust #1 is sued by the tenant the liability flows to the beneficial owner, or XYZ, LLC.

Now if XYZ, LLC were on title to the property instead of the land trust, the liability would be contained within that one LLC. But in our design flawed structure, the liability flows from the land trust into the LLC. What does the LLC own? Not only Land Trust #1 but also Land Trust #2 and Land Trust #3. So the tenant can also get what the LLC owns, which is equity in all three land trusts. “Well,” says the land trust promoter as they prepare to move to Alaska, “that didn’t work either.”

As is clear, the design of your asset protection plan really does matter. When building it listen to your little voice, the one that is always there and always protective. If the proposed plan doesn’t make sense, if it doesn’t add up, think again. Get another opinion. Your asset protection is too important to be left to unquestioned amateurs.

Corporate Direct, on the other hand, does not advise using land trusts or any overly complicated structures. We have been in the business of asset protection for over 30 years and we can help you structure your entities correctly and in a straight forward and affordable manner. Get your free 15-minute consultation to get started today!

Corporations have been used for over 500 years to limit owners’ liability and thus encourage business investment and risk taking. Their use for this purpose continues to this day.

Corporations have been used for over 500 years to limit owners’ liability and thus encourage business investment and risk taking. Their use for this purpose continues to this day.