Real estate investors and business owners always run the risk of being sued. If they’re not protected, a courtroom loss can lead to a loss of personal assets. Even if they use a strong LLC, the victor in a car wreck case, for example, may try to get a charging order. And if their holding LLC owns an operating LLC, that same winner may try and get a cascading charging order against one or more operating LLCs. If they succeed with this remedy, it could really harm business owners. But first, what are charging orders and cascading charging orders, and what do they do?

What is a Charging Order?

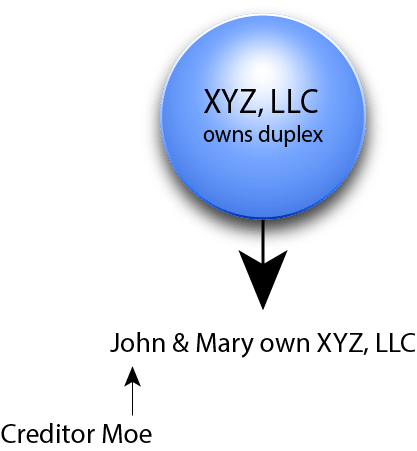

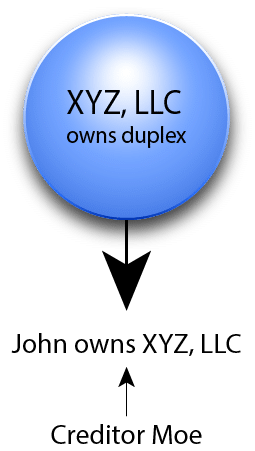

A charging order is simply a lien on distributions from a business. So, if any distributions are made to the LLC owner, the person with the charging order will get them instead. The court ‘charges’ the LLC owner to make distributions to the car wreck victim. But when would this apply? Here is a chart to help explain this concept:

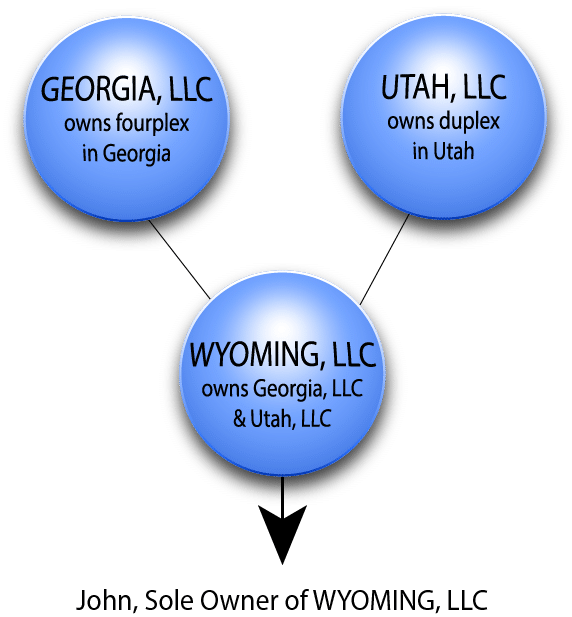

In this chart, Joe owns a Wyoming LLC. That Wyoming LLC owns two operating LLCs. Wyoming is a stronger asset protection state, where the charging order is the exclusive remedy.

Now let’s say that Joe got into a car accident. If the car wreck victim were to sue Joe and win, they could get a charging order on Joe’s Wyoming LLC. The chart below explains this concept:

However, the charging order limits what that car wreck victim can do. They don’t have the right to manage Joe’s business. And they don’t have the right to demand or vote that Joe’s business pay them. The only way they get paid is if Joe makes a distribution from the entity. And if Joe doesn’t make any distributions, the car wreck victim doesn’t get paid. As you can see, the charging order is a very powerful tool for protection.

What is a Cascading Charging Order?

Now that we discussed what a charging order is, what exactly is a cascading charging order? And how does it differ from a regular charging order?

With a regular charging order, the car wreck victim can place it on any businesses that Joe directly owns. However, a cascading charging order is different. This applies where the car wreck victim tries to place a charging order on the operating companies that Joe indirectly owns.

While Joe doesn’t directly own the operating LLCs, the car wreck victim may still try to place a cascading charging order on it. This is because Joe indirectly owns the operating LLC through Joe’s direct ownership of the Wyoming LLC. The diagram below illustrates this concept:

But can the car wreck victim do this? One recent Texas case addressed this issue.

Bran v. Spectrum MH, LLC

One recent Texas case, Bran v. Spectrum MH LLC, dealt with this issue.[1] In Bran, the parties settled the dispute through arbitration. The arbitrator ruled in favor of Spectrum, and awarded a judgment worth $1.5 Million against Bran.

To collect this judgment, Spectrum appointed a receiver. What the receiver did next was deemed to be out of line. Instead of placing a charging order against the businesses that Bran directly owned, the receiver reached the accounts of businesses that Bran indirectly owned. Bran then filed an emergency appeal.

On appeal, the issue before the Texas Court of Appeals was whether the receiver could get a cascading charging order to reach the assets of the businesses that Bran indirectly owned.

The Court of Appeals ruled that the receiver could not. Instead, the receiver could only reach the assets that Bran directly owned. The court also noted that before the receiver could attach a charging order against a specific entity, Spectrum must prove that Bran had an ownership interest in those entities. This means that if Bran indirectly owned an interest in an entity, the receiver could not reach that entity’s assets.

In Bran, the cascading charging order was off limits. The court also mentioned that the charging order was the exclusive (or only) remedy that the receiver had. This means that the receiver could only collect the $1.5 Million judgment from assets that Bran directly owned.

What This Means For You

Many real estate investors and business owners have an entity structure where they directly own one holding entity, and that entity owns one or more operating entities. When the business owner is sued personally, some courts (like Texas) have held that a person can’t reach that second entity via the cascading charging order.

This structure that involves a Wyoming holding company is very advantageous for business owners, because it limits what a creditor can collect when they are personally sued. And because courts are beginning to block these cascading charging orders, having this structure is a great asset protection strategy.

[1] Bran v. Spectrum MH LLC, 2023 WL 5487421 (Tex.App., 14th Distr,, August 24,. 2023).

")