When states raise their fees, people vote with their feet. We described Nevada’s new corporate fees in our last issue (a jump from $325 a year to $650.) We also described how you could ‘continue’ your Nevada entity (or any state entity for that matter) into Wyoming, where the annual fee is just $50.

Continuance is an easy process — unless the state of California is involved.

If your current company is a Nevada company qualified in California you may want to file a continuance out of Nevada and into Wyoming. If so, you will need to notify the state of California that your domestic laws have changed (meaning you are a Wyoming, not a Nevada, company).

The only way the state of California will accept the change of your domestic laws is via requalification after the dissolution in California. So you dissolve in California and then come back as a Wyoming entity (no other state requires this step).

The cost for all the California fees and work is $626. The cost of the continuance from Nevada to Wyoming is $995. The total is $1,621. But you are saving $600 a year (the $650 Nevada fee less the $50 Wyoming fee.) That $1,621 pays for itself in 2.7 years.

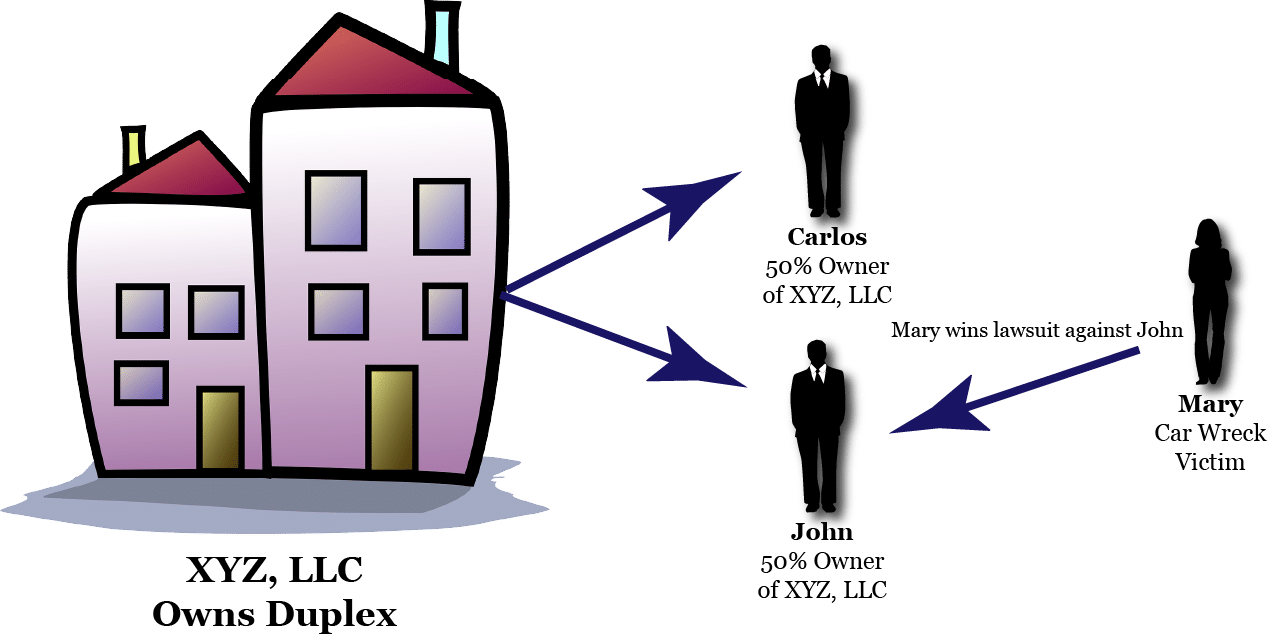

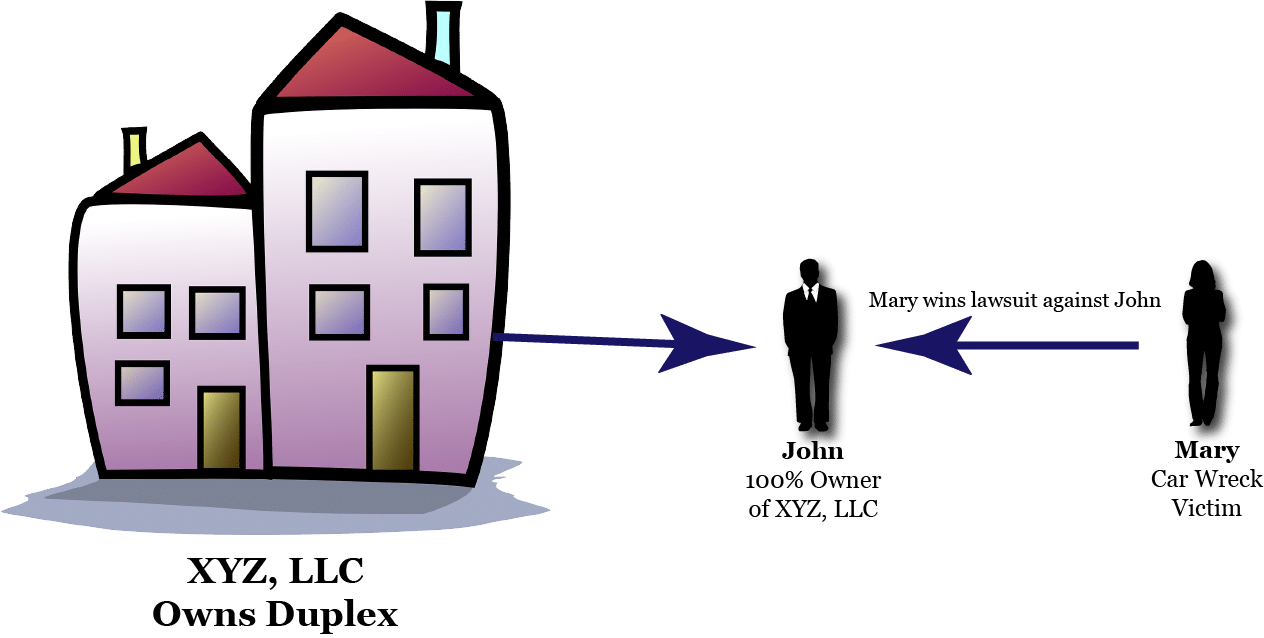

Some clients are sticking with their Nevada corporations because Nevada is the only state in the Union to provide charging order protection for corporate shares. This is worthwhile asset protection, and is worth the extra cost for some clients.

Others are continuing into Wyoming to save $600 a year. Our role is to inform you of your options. Whether to continue out of Nevada to Wyoming or not is a judgement call on your part.

Enjoy your summer.

Garrett Sutton, Esq., author of Start Your own Corporation, Run Your Own Corporation, Loopholes of Real Estate, The ABC’s of Getting Out of Debt, Writing Winning Business Plans and Buying and Selling a Business in the Rich Dad Advisors series, is an attorney with over twenty-five years experience in assisting individuals and businesses to determine their appropriate corporate structure, limit their liability, protect their assets and advance their financial, personal and credit success goals.

Garrett Sutton, Esq., author of Start Your own Corporation, Run Your Own Corporation, Loopholes of Real Estate, The ABC’s of Getting Out of Debt, Writing Winning Business Plans and Buying and Selling a Business in the Rich Dad Advisors series, is an attorney with over twenty-five years experience in assisting individuals and businesses to determine their appropriate corporate structure, limit their liability, protect their assets and advance their financial, personal and credit success goals.