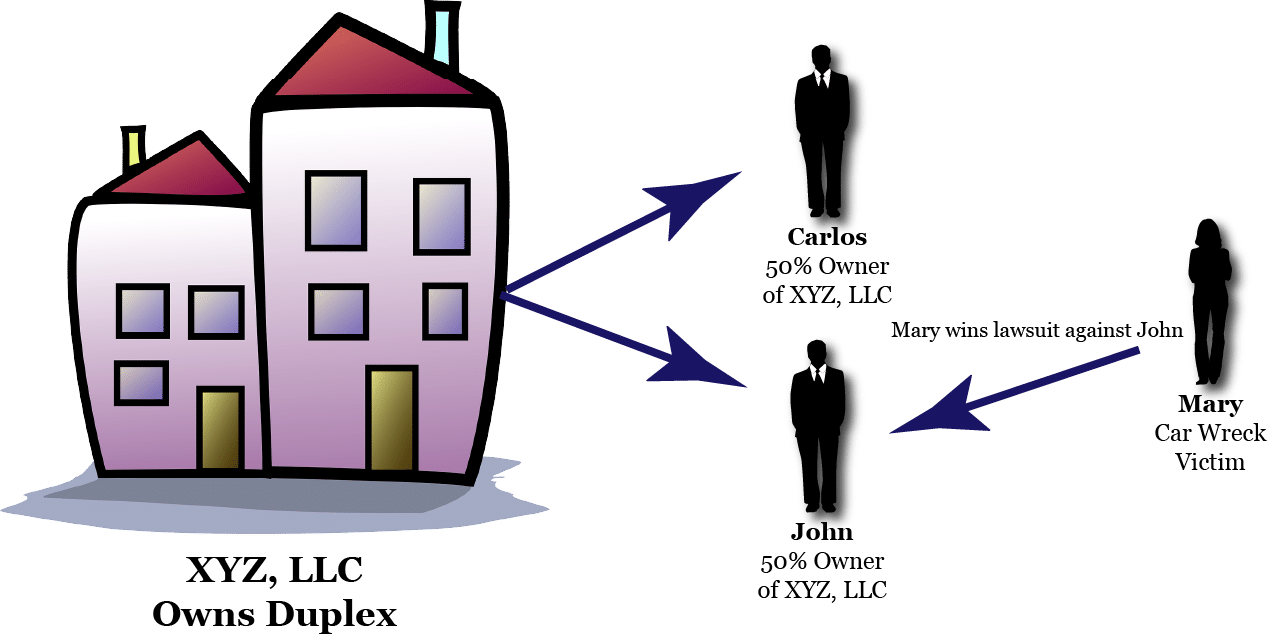

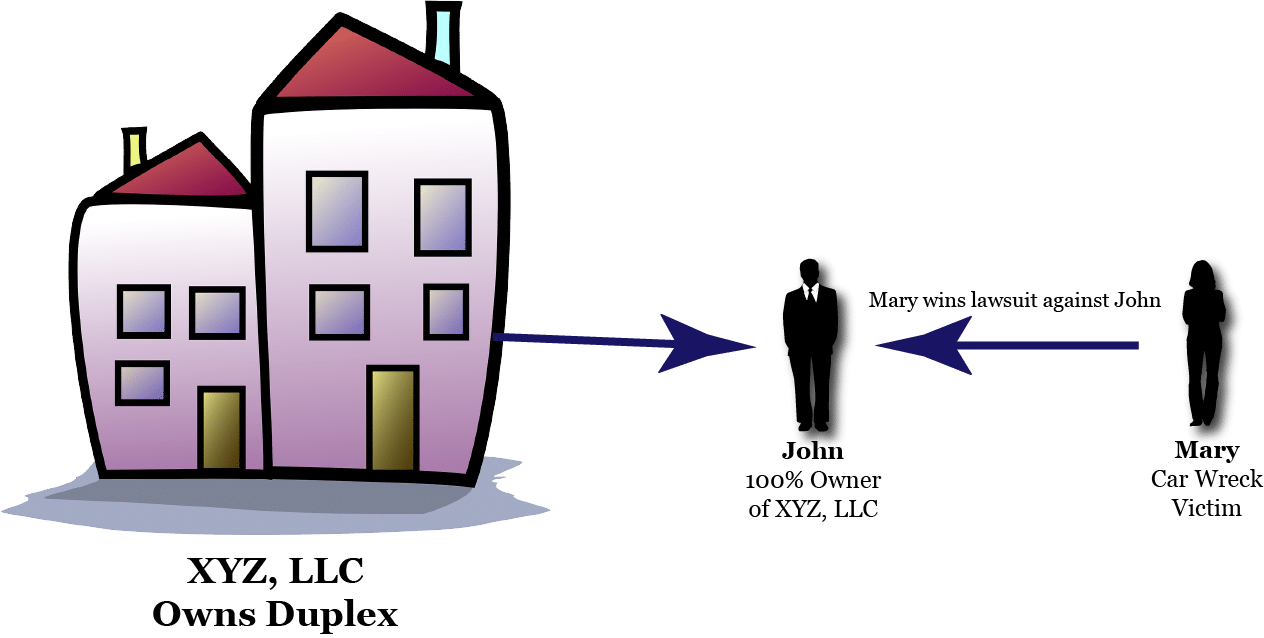

New Court Case May Indicate Future Requirements

Winn-Dixie, a large supermarket chain, was sued under the Americans with Disabilities Act (ADA). Juan Gil, a blind Florida resident, went to court because the chain’s website was not accessible to him.

The ADA requires that places of public accommodation provide “full and equal enjoyment of the goods, services, facilities, privileges, advantages, or accommodations of any place of public accommodation.” The U.S. District Court Judge for the Southern District of Florida relied upon previous court holdings that the ADA covered both tangible and intangible barriers that restrict individuals with disabilities from the enjoyment of a public accommodation’s service. Since the supermarkets’ website did not accommodate the visually impaired, it denied Mr. Gil “the full and equal enjoyment of Winn-Dixie’s goods, services, facilities, privileges, advantages, or accommodations because of his disability.”

The court issued an injunction requiring Winn-Dixie to make its website accessible to the disabled. A new standard has emerged known as the Website Content Accessibility Guidelines (WCAG), version 2.0. Screen reader technologies can now read website content to individuals with blindness and assist them in navigating the site with voice prompts. Integrating such technologies into a “public” website will help satisfy the new and developing WCAG requirements.

Is your website ADA compliant? Hotels, restaurants, retailers and other places of public accommodation that transact business with the public over their website should take note. If not now, at some point in the future you may be required to bring your website into compliance with WCAG 2.0.

Garrett Sutton, Esq., author of Start Your own Corporation, Run Your Own Corporation, Loopholes of Real Estate, The ABC’s of Getting Out of Debt, Writing Winning Business Plans and Buying and Selling a Business in the Rich Dad Advisors series, is an attorney with over twenty-five years experience in assisting individuals and businesses to determine their appropriate corporate structure, limit their liability, protect their assets and advance their financial, personal and credit success goals.

Garrett Sutton, Esq., author of Start Your own Corporation, Run Your Own Corporation, Loopholes of Real Estate, The ABC’s of Getting Out of Debt, Writing Winning Business Plans and Buying and Selling a Business in the Rich Dad Advisors series, is an attorney with over twenty-five years experience in assisting individuals and businesses to determine their appropriate corporate structure, limit their liability, protect their assets and advance their financial, personal and credit success goals.