Is a Decentralized Autonomous Organization (DAO) Right For You?

A DAO is an organization operated by a smart contract, which is a computer code running within the blockchain. The ‘A’ for Autonomous refers to the self-executing nature of it all. If a condition is met the computer code executes the transaction. There is no need for human managers, with all their failings, to be involved. The contract provides management certainty.

The DAO concept is advocated as a benefit for those from around the world with common goals who may not know or trust each other. You come together for a common project and the smart contract guides the beneficial way.

But there is one big problem with an ordinary DAO: There is no asset protection. Essentially, you and all of your like-minded DAO compatriots are operating as general partners, with unlimited personal liability.

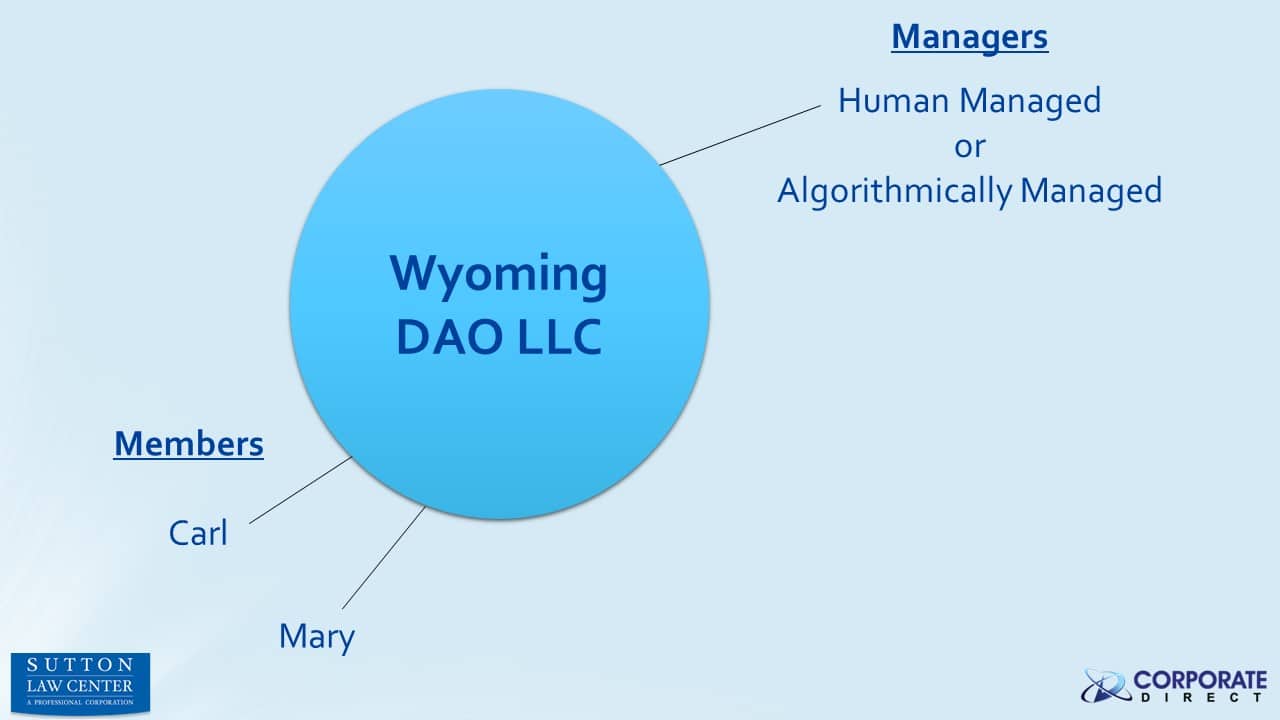

Hence, the Wyoming DAO LLC.

The state of Wyoming is on a mission to be the best jurisdiction for all things blockchain. And in realizing that a DAO had a legal gap, they had their legislature provide a legal solution. A DAO can now be organized as a Wyoming LLC. You and your partners can now autonomously operate with the solid protection of Wyoming’s very strong LLC laws.

The requirements aren’t difficult. You need to have a Wyoming registered agent and pay the annual state fees. Your official LLC name must include the wording ‘DAO LLC,’ as in Betty’s Plumbing DAO, LLC. You can list yourself, a human, as a manager or you can choose to be algorithmically managed. Meaning your DAO LLC can be managed by artificial intelligence – or AI. Who thought science fiction would ever come to corporate governance?

But therein lies the largest detraction to the DAO LLC. By being algorithmically managed via a smart contract (which is your own LLC’s Operating Agreement) you are giving up some privacy.

Smart contracts operate on the blockchain. And the blockchain is out there for all to see. So by knowing the entity name – Betty’s Plumbing DAO, LLC – for example, someone can go online to read Betty’s Operating Agreement. They can access her operational road map and internal strategies.

Many of our clients prefer their entity’s governance to remain confidential. So when it comes to balancing autonomous with anonymous, privacy wins. A human manager following a confidential Operating Agreement is preferred by most.

To date, we have not formed any DAO LLCs due to this privacy limitation. It will be interesting to see if and when the state of Wyoming deals with this gap in an otherwise unique and useful corporate structure.

Learn more about writing successful business plans from Garrett Sutton’s Book,

Learn more about writing successful business plans from Garrett Sutton’s Book,  Corporations have been used for over 500 years to limit owners’ liability and thus encourage business investment and risk taking. Their use for this purpose continues to this day.

Corporations have been used for over 500 years to limit owners’ liability and thus encourage business investment and risk taking. Their use for this purpose continues to this day.